Executive Summary: A judgment lien court records API lets underwriting teams surface money judgments against a borrowing business before funding, because a docketed money judgment can attach as a lien to the debtor's property and reorder who recovers first.[1][2] This guide shows how a lender uses court-records data to find judgments against a business in New York and Miami-Dade, route the file by judgment count, amount, and recency, and apply an explicit fallback everywhere else.

Why does a judgment lien matter before funding?

What does a docketed judgment do to collateral?

A money judgment is not just a number on a docket. Once a creditor dockets it in the right county, the judgment can create a lien that attaches to real property the debtor owns there, giving that creditor a claim ahead of later interests.[1] For a lender about to advance funds, that means the recovery value behind the deal may already be spoken for.

The signal that matters is not a single old, satisfied judgment. It is a pattern: multiple open judgments, large unpaid amounts, or a recent filing that the borrower did not disclose. Those patterns change whether the file stays automated, moves to manual review, or pauses.

Why is self-reported litigation not enough?

A borrower has every incentive to omit a judgment, a disputed claim, or a recent suit. A direct search of the court record gives the lender an independent control that does not depend on what the applicant chose to disclose on the application.

The question before funding is not whether the applicant says there is no judgment against the business. The question is whether the public court record supports that before money moves.

What does the Court Records API actually cover?

Which jurisdictions are in scope?

Cobalt's Court Records API covers New York State and Miami-Dade County, Florida only. It is targeted coverage, not nationwide litigation screening. Those two venues concentrate a large share of alternative-lending and MCA activity, which is why the coverage is narrow but useful for this ICP.

What does the API not cover?

The API does not query PACER or federal courts, and it does not return bankruptcy records or other states. A federal case file is a docket sheet plus the documents filed in the matter, accessible through the federal system rather than a state venue.[6] PACER is the federal baseline for court records and holds access to a very large volume of documents, but it is industry context here, not Cobalt coverage.[3] State court systems are fragmented across thousands of venues, and the large majority of cases are handled at the state level, which is exactly why no single targeted API covers everything.[2]

How does Cobalt return judgment data in the workflow?

What does the API call look like?

The Court Records API is asynchronous. Every request needs `businessName`, `jurisdiction` (`newYork` or `miamiDade`), and a `callbackUrl`. Results are POSTed to the callback when ready, usually within 30 to 120 seconds. Search is by business name only.

curl --location 'https://apigateway.cobaltintelligence.com/courtCases?businessName=Acme%20Capital%20LLC&jurisdiction=newYork&callbackUrl=https%3A%2F%2Fyour-app.com%2Fcobalt-callback' \

--header 'x-api-key: YOUR_API_KEY' \

--header 'Accept: application/json'What fields come back?

The response can include judgment details such as type and status, case information including case number and court division, filing dates, parties involved, and judgment amounts where available. Amounts are not always present, so the workflow must treat a missing amount as unknown, not as zero.

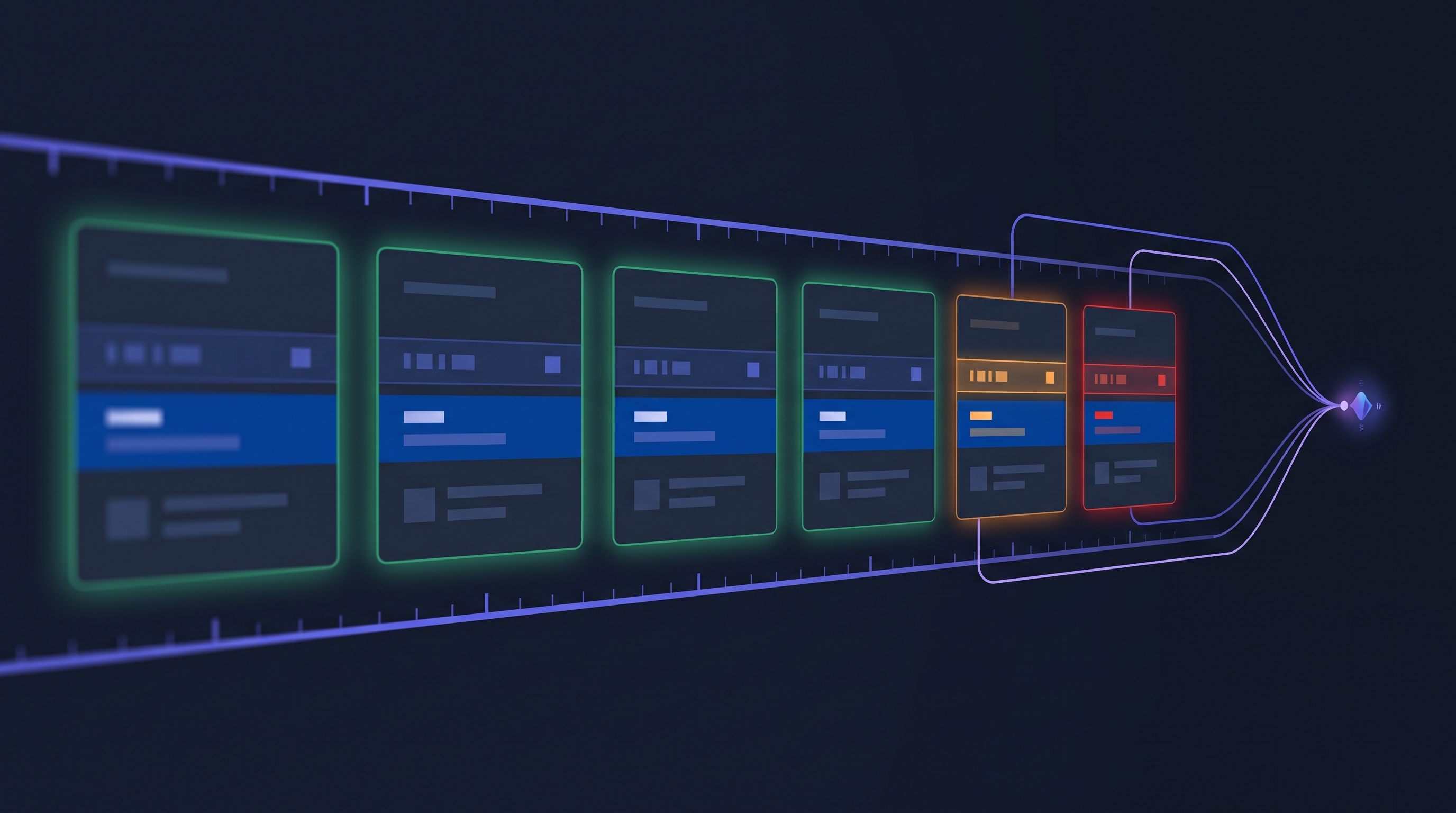

What routing rules turn judgments into actions?

How should a lender score the result?

A first policy pass can stay simple. No open judgment found in a supported venue lets the file continue. One small, old, satisfied judgment continues with a note. Multiple open judgments, a large unpaid amount, or a judgment filed close to the application date should pull the file into review or a funding hold.

| Signal | Workflow action | Why it matters |

|---|---|---|

| No judgment found (supported venue) | Continue automated underwriting | No docketed money judgment surfaced in covered data |

| One small satisfied judgment | Continue with note | Resolved claim, limited bearing on recovery |

| Multiple open judgments | Manual review | Pattern of unresolved claims against the business |

| Large unpaid amount | Manual review or hold | Judgment lien may sit ahead of the lender on assets |

| New judgment within 90 days | Funding hold | Recent claim may not yet appear in credit or bank data |

| Unsupported jurisdiction | Fallback search | No silent clearance when coverage does not reach the venue |

What should the exception queue show?

The exception queue should display the case numbers, judgment amounts where available, filing dates, party names, and the exact rule that fired. An underwriter should not have to reopen a court website to understand why the file paused.

How should judgment data be used responsibly?

What does FCRA restrict here?

When court or judgment data flows into how a credit decision is made, the lender takes on responsibilities under the Fair Credit Reporting Act. Civil judgments that antedate a report by more than seven years, or until the governing statute of limitations runs, whichever is longer, are restricted from consumer reports.[4] Treat stale judgments with care and set policy with counsel.[5]

Why is Cobalt a data source, not a decision?

Cobalt returns the court data; the lender owns the rule that turns a judgment into an accept, condition, or decline. The same judgment can mean different things for a $25,000 advance and a $500,000 facility, so the threshold logic stays with the lender.

How does this fit a complete pre-funding stack?

What should run alongside court records?

Court data is strongest paired with entity verification, TIN/EIN matching, UCC lien discovery, and OFAC screening. Entity data confirms the business exists and is active. UCC filings show secured claims on assets. Court records add the judgment and litigation layer. Read the pre-funding UCC lien search underwriter workflow for the lien side of the same file.

Where should the judgment check sit?

Place the court-records check before final approval and before funding, after the legal name is normalized. A judgment found after funding is only a postmortem. For the sanctions and AML layer, see BSA/AML for alternative lenders and OFAC's role.

What implementation checklist should teams use?

What should the first production version include?

1. Verify the legal entity name and confirm the business is active.

2. Determine whether the venue is New York or Miami-Dade.

3. Call `GET /courtCases` with the business name, jurisdiction, and callback URL.

4. Parse judgment count, amounts where available, dates, and parties.

5. Apply routing rules before final approval.

6. Store the raw response, parsed flags, timestamp, and reviewer notes.

7. Send any unsupported venue to a documented fallback search, never a silent clear.

How can a lender start using court-records data?

Begin where your borrowers concentrate, New York and Miami-Dade, and wire the business-name lookup into the pre-funding hold point so a judgment can still change the decision. To see the call and response against your own test cases, book a Cobalt demo and bring a few business names you want to screen.

.png)