Executive Summary: Cobalt EIN Verify vs Middesk Identity: Lender Comparison is a practical control for lender product, risk, and engineering evaluators. The core question is simple: does the business name on the application belong with the tax identification number being used for the account, payment, or credit decision? The IRS TIN Matching program is built around name and taxpayer identification number validation before eligible information returns are filed.[1] Lenders and financial platforms can use the same name/TIN logic earlier in the workflow, before a deal is funded or a business account is activated. For vendor comparison, the risk is comparing a narrow IRS name/TIN validation check with broader KYB identity platforms. A Secretary of State record may show that an entity exists, but it does not prove that the submitted EIN belongs to the applicant. Cobalt's TIN/EIN Verification API is intentionally narrow: the customer provides both `tin` and `businessName`, and the API validates whether that pair matches IRS records. That narrow answer is useful because it can be routed automatically.

Why cobalt EIN vs middesk identity Matters

The identity check belongs before operational commitment. In this workflow, that means before vendor evaluation, proof of concept design, risk policy mapping, and cost review. If the name and EIN do not match, the team still has time to request a W-9, compare the legal name from the state filing, check whether the applicant used a DBA, and decide whether the mismatch is benign or suspicious.

IRS Form W-9 instructions exist because payers need accurate taxpayer identification information before reporting and withholding obligations become a problem.[2] The CP2100 and CP2100A notice process shows the cost of waiting until after reporting: incorrect name/TIN combinations can trigger correction work and backup withholding procedures.[3]

That is why EIN verification should not be treated as a back-office cleanup step. It is a pre-decision identity signal.

What the API Should Validate

A lender or platform should not ask an EIN verification product to do everything. The correct job is limited and specific:

• Confirm that the submitted business name and EIN match IRS records.

• Return a structured IRS code that can drive workflow routing.

• Preserve the check timestamp for audit review.

• Report whether the IRS service was available at the time of the check.

• Keep discovery questions separate from validation questions.

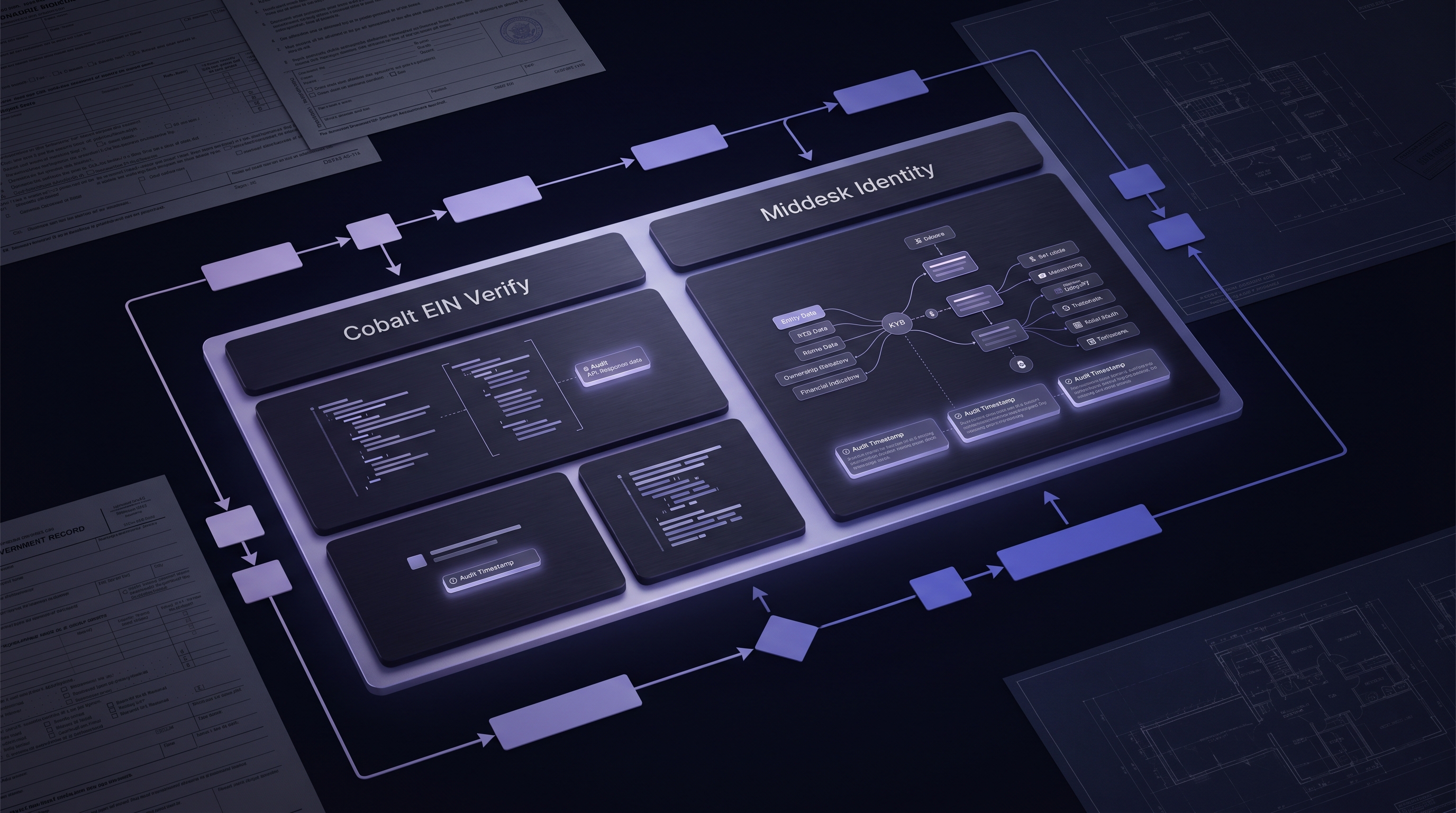

Cobalt's product docs describe the endpoint as `GET /tinVerification`, with two required parameters: `tin` and `businessName`. A clean match returns a status, IRS code, reason, service status, and last IRS check date. It is validation, not EIN discovery.

How to Route Match and No-Match Results

The routing rule should be written before the API goes live. A simple starting policy looks like this:

• Code 0, match: continue the normal workflow.

• Code 1, TIN not issued: stop or request corrected tax documentation.

• Code 2, TIN issued but name does not match: request W-9, compare the SOS legal name, and route to manual review.

• Code 3, incomplete IRS records: do not auto-approve based on the tax ID check alone.

• IRS unavailable: queue a retry instead of silently skipping the check.

A mismatch is not always fraud. It can happen because the applicant used a DBA, abbreviated a legal suffix, changed names recently, or typed the wrong value. But it is always a reason to pause the automated path.

How It Fits With KYB and Compliance

FinCEN's Customer Due Diligence rule focuses on written procedures for identifying and verifying customers and beneficial owners.[4] EIN verification does not replace those procedures. It supports them by documenting that the business tax identity was checked at the time of onboarding or funding.

The strongest workflow pairs EIN verification with Secretary of State verification. The SOS check confirms the entity exists and provides the state-registered legal name. The EIN check confirms whether that legal name matches the submitted federal tax ID. Together they catch more risk than either check alone.

Federal Reserve Financial Services has warned institutions to apply synthetic identity fraud lessons to synthetic business fraud, especially where business formation and onboarding processes can be abused.[5] EIN verification is one of the cleanest controls for that exact gap.

Implementation Checklist

For vendor comparison, use this implementation checklist:

1. Normalize the EIN to nine digits with no dash.

2. Pull the legal business name from the application and, when possible, from the SOS result.

3. Call the EIN verification endpoint before final approval or activation.

4. Store the submitted name, submitted EIN, IRS code, IRS reason, service status, and timestamp.

5. Map every response code to a decision path.

6. Give analysts a short reason code, not a raw JSON blob.

7. Retry service-unavailable responses instead of approving around them.

The goal is not to add another manual step. The goal is to remove manual ambiguity from the few cases that actually need human review.

Common Failure Modes

The most common failure is using EIN verification too late. Once the account is active or the funds are sent, the team has less leverage to correct documents or stop risk. Another failure is treating Code 2 as an automatic fraud conclusion. That creates false positives. The better policy is to make Code 2 a documented review path.

A third failure is asking the API to discover unknown EINs. That is not what a validation product does. The applicant must provide the EIN, and the system must validate whether the name and EIN belong together.

Bottom Line

Cobalt EIN Verify vs Middesk Identity: Lender Comparison is not just a compliance detail. It is a workflow control. It helps lender product, risk, and engineering evaluators catch mismatched business identity data before approval, funding, onboarding, or payout. Cobalt's TIN/EIN Verification API gives teams a structured IRS-backed signal that can be routed in seconds and preserved for audit review.

.png)