Executive Summary: An automated underwriting system (sometimes called an automated underwriting platform, or AUS / AUP) is software that pulls applicant data, runs it through risk rules and machine learning models, and returns an instant credit decision. For mortgage and insurance carriers, these systems have been mature for decades. For small business and alternative lenders, the picture is messier. Most automated underwriting platforms on the market in 2026 were built for W-2 borrowers or insurance applicants. If you write merchant cash advances, fintech term loans, equipment financing, or lines of credit to small businesses, the off-the-shelf options leave a verification gap that creates fraud risk on one side and unnecessary declines on the other. This guide walks through what is actually available, what to look for, what every system gets wrong about small business data, and how to decide between buying a platform and building one with verification APIs.

The state of automated underwriting in 2026

Automated underwriting has moved well past its origins as a Fannie Mae rules engine. Modern systems combine traditional rules with machine learning, document extraction, and real-time data orchestration. Vendor-published efficiency claims for these systems vary widely (Camunda, ScienceSoft, and individual platform vendors have published process-time reductions in the 50% to 70% range, almost all of it from mortgage and insurance deployments). Treat those numbers as directional, not as something to put in a credit committee deck.

The reason the mortgage and insurance numbers do not transfer cleanly to small business and alternative lending is structural. A consumer mortgage applicant has a credit score, a W-2, and a bank statement. A small business applicant has an entity, an owner, a state filing, possibly a UCC lien, possibly a court judgment, and cash flow that does not look anything like W-2 income. The platforms built for mortgage simply cannot ingest those data sources natively, which is why off-the-shelf adoption among MCA shops and ABL lenders has been slow even as the technology matured.

What is an automated underwriting system (and how is it different from a platform)?

The terms automated underwriting system and automated underwriting platform are used interchangeably across the industry. Investopedia defines automated underwriting as the use of algorithms and statistical models to evaluate loan applications and produce a recommendation, typically Approve, Decline, or Refer for manual review. Fannie Mae's Desktop Underwriter (DU) and Freddie Mac's Loan Product Advisor (LPA) are the canonical examples in mortgage lending.

If there is any meaningful distinction in 2026 usage, it is this. "System" tends to refer to the decisioning engine itself, the rules and models that produce the verdict. "Platform" tends to refer to the broader software stack around the decisioning engine, including the loan origination system, document handling, applicant portal, and integrations with data providers. In practice, when a vendor says their automated underwriting platform does X, they almost always mean their underwriting system inside their platform does X. We will use the terms interchangeably in the rest of this guide.

What every automated underwriting system, regardless of label, has to do is the same four-step workflow:

1. Data retrieval. Pull applicant and entity data from internal forms and external APIs (credit bureaus, bank statements, public records, business registries).

2. Algorithmic analysis. Apply rules, scorecards, and machine learning models to assess risk factors.

3. Instant decisioning. Return Approve, Decline, or Refer in seconds.

4. Audit and compliance. Generate timestamped trails for every decision, defensible against regulator and litigation review.

Why mortgage and insurance underwriting platforms fail small business and alt-lending

The platforms most often cited when someone searches "automated underwriting system" were not designed for the small business lending workflow. Four specific gaps show up over and over in our work with alternative lenders.

1. Built for W-2 income, not merchant cash flow

Mortgage AUSes assume applicants have steady, documented W-2 income. MCA providers and SMB lenders assess businesses where revenue is daily, irregular, and tied to merchant processor data, bank deposits, or invoice payments. Generic platforms either refuse to score these applicants or score them incorrectly, treating cash flow volatility as risk when it is just the nature of small business revenue.

2. They skip primary-source business verification

Most off-the-shelf platforms verify identity using consumer credit bureau pulls. They do not natively pull from state Secretaries of State to confirm the legal entity exists, is in good standing, has the right registered agent, or is owned by the person filling out the form. This is the single most exploited gap in small business lending fraud. Synthetic identities and shell entities slip through systems that never check the primary source.

3. They underweight UCC and existing liens

For asset-based lending, equipment finance, and MCA, knowing whether a business already has UCC filings against it is fundamental. Many automated platforms either do not pull UCC data at all or pull it from stale aggregator databases that miss recent filings. By the time you fund the loan, you find out you are in second position behind a competitor.

4. No real-time SOS lookups

Secretary of State data changes constantly. A business in good standing on Monday can be administratively dissolved on Friday for failing to file an annual report. Automated underwriting systems that rely on cached or quarterly-refreshed business registry data make decisions on stale facts. For real-time decisioning to mean anything, the verification data has to be real-time too.

Comparison: 7 automated underwriting platforms for small business and alternative lending

Here is how the platforms most often considered by SMB and alt-lenders stack up. None of these is the "best" in absolute terms, because the right answer depends on your loan product, volume, and existing data infrastructure.

| Platform | Best for | Strength | Gap for SMB / alt-lending |

|---|---|---|---|

| LoanPro | Modern lending, full LMS | End-to-end loan management plus decisioning. Strong API surface. | Generic verification layer. Does not natively pull primary-source SOS data. |

| TurnKey Lender | Mid-market lenders | Configurable scorecards. Good UX for non-technical risk teams. | Limited primary-source business data. Built more for consumer than SMB. |

| Zest AI | Consumer credit decisioning | Best-in-class machine learning, fairness testing, explainability. | Consumer-first. Weak on SMB entity verification. Bring your own business data. |

| Heron Data | Cash flow analysis from bank statements | Excellent transaction parsing and categorization. | No business entity verification. Pairs well with a verification layer rather than replacing one. |

| Docsumo | Document automation | OCR and structured extraction from PDFs and images. | Document layer only. Not a decisioning engine. |

| Underwrite.ai | AI-only decisioning | Continuous model retraining. Strong on alternative data signals. | BYO data sources required. You still need a verification layer feeding it. |

| Blooma | Commercial real estate | CRE-specific automation, loan sizing, credit memo generation. | Not applicable to SMB term lending or MCA. |

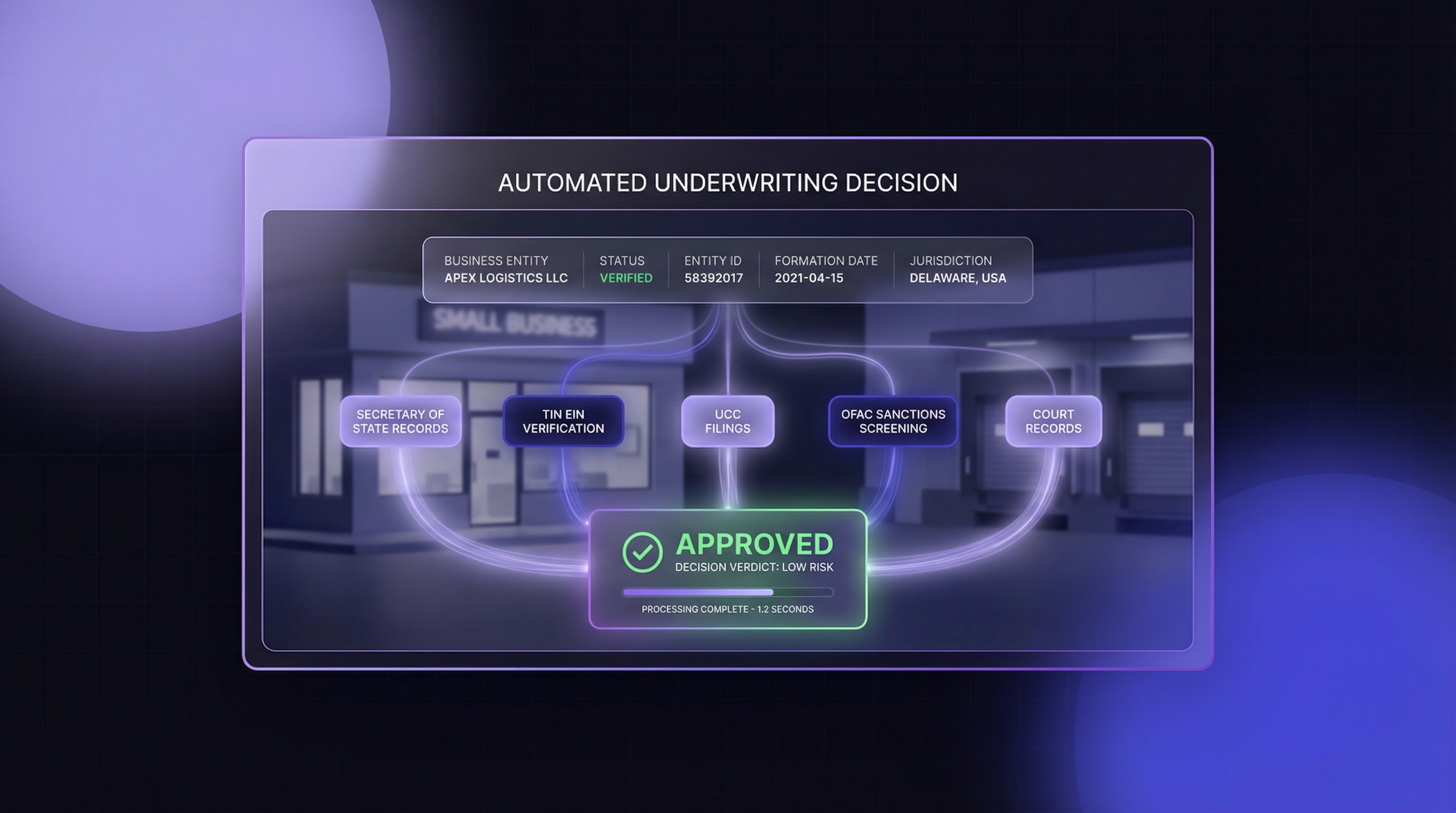

| Cobalt Intelligence | Verification data layer for any AUP or in-house build | Real-time SOS, TIN/EIN, UCC, OFAC, court records sourced directly from primary sources. | Not an automated underwriting system itself. Pairs with one or powers an in-house build. |

Why Cobalt is in a separate row: We are not an automated underwriting platform. We are the verification data layer that every automated underwriting system needs as input. The seven platforms above all do something Cobalt does not, which is run the actual decisioning logic. Cobalt does something the seven do not, which is verify business entities against primary sources in real time. The honest answer for most alt-lenders is "pick one of the seven for decisioning, plug Cobalt in for verification."

The data layer every automated underwriting system needs

Whichever platform you pick, or whether you build your own, the quality of the decision is bounded by the quality of the data going in. Here are the five data sources every small business automated underwriting system needs, and why most platforms fall short on the last three.

1. Credit bureau data

Personal and business credit pulls from Experian, Equifax, TransUnion, and Dun & Bradstreet. Every platform handles this. It is necessary but not sufficient for SMB lending because business credit files are often thin or missing entirely.

2. Bank statement and cash flow data

Pulled via aggregators like Plaid, MX, or parsed by tools like Heron Data. This tells you whether the business actually generates revenue and what the deposit volatility looks like.

3. Business entity verification

Real-time confirmation that the legal entity exists, is in good standing, has the right registered agent, owners, and address. Sourced from Secretary of State filings across all 50 states. This is where most platforms fall short. Many use cached aggregator data that lags primary sources by weeks or months. Pulling directly from SOS records, the way Cobalt's verification API does, is the difference between catching a synthetic entity at application time and discovering it at default.

4. UCC filings

Existing liens against the business or its assets. For asset-based lending, equipment finance, and MCA, this is non-negotiable. Like SOS data, UCC filings must come from primary sources to be reliable.

5. OFAC, sanctions, and court records

Sanctions screening is required for compliance. Court records (judgments, bankruptcies, civil suits) are required for risk. Both must be matched against the verified entity and verified owners, not against names typed into a form.

Items 3, 4, and 5 are where most off-the-shelf platforms underinvest, and they are the items most likely to determine whether a small business deal performs or defaults. Whether you address that gap by adding a verification API to your existing platform, building an in-house pipeline, or pressuring your current vendor to expose better primary-source feeds, the gap itself is the thing to fix first.

Build vs buy: when to license a platform vs build with verification APIs

The classic build-vs-buy trade-off shows up sharply in automated underwriting. Here is the honest split.

Buy a platform when:

• You write under 200 applications per month.

• Your risk profile is generic enough that a configurable platform can model it well.

• You do not have an engineering team capable of maintaining a decisioning service.

• You want to be live in weeks, not months.

• Compliance reporting is more valuable to you than model customization.

Build with verification APIs when:

• You write more than 200 applications per month and unit economics matter.

• You serve a niche vertical that off-the-shelf platforms model badly (specialty MCA, equipment finance for a single industry, invoice factoring).

• You have data scientists or risk engineers who want full control over feature engineering and model retraining.

• You already have a loan origination system and just need the decisioning layer.

• You consider your underwriting model a competitive moat.

The middle path most growing alt-lenders settle on is "buy a platform for decisioning, own the verification layer." The decisioning engine becomes somebody else's problem to maintain. The data feeding it is yours, sourced from primary records, refreshed in real time, and audit-ready under examination. That split is where most healthy underwriting stacks end up after two or three years of iteration.

What to actually ask any automated underwriting vendor

Skip the table-stakes questions. Audit trails, sandbox access, and SLAs are things any moderately experienced ops director already asks on every vendor call. The questions below are the ones that actually separate good vendors from bad ones, and the ones most likely to expose a coverage gap that will hurt you eight months in.

1. Where does your business entity verification data come from, state by state? "An aggregator" is not an answer. Ask for the specific source for at least five states where you write meaningful volume, and ask how often each state refreshes. Real-time direct-from-SOS sources update on every query. Aggregator sources can lag the actual filing by weeks or months. If a vendor cannot tell you which states are real-time and which are cached, assume the worst.

2. For OFAC and sanctions screening, are you matching against verified legal owners or against names typed into a form? This is the single biggest compliance gap in small business automated underwriting. Name-only matching catches the obvious cases and misses the ones that matter. The right answer is that the vendor pulls verified ownership from primary sources, then runs OFAC against those verified entities. If they cannot describe that flow, the audit risk is yours.

3. For UCC filings, do you return secured party and collateral description, or just a hit/no-hit flag? A flag tells you nothing. A full record tells you whether you are about to fund into second position behind a competitor and what the senior collateral looks like.

4. What is your model retraining cadence, and who has visibility into the features? Black-box models are a regulator problem waiting to happen, especially under fair lending review.

5. Can I see one real customer reference at our volume tier and loan type? Not the platform's biggest logo. A reference at your scale, in your vertical, willing to talk candidly. If the vendor cannot produce one, the use case is unproven.

Ready to plug a real verification layer into your underwriting stack?

Cobalt's verification API delivers real-time SOS, TIN/EIN, UCC, OFAC, and court records to any automated underwriting platform or in-house build. 50-state coverage, primary sources, audit-ready.

.png)